Licencia Creative Commons

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-SinDerivadas 4.0 Internacional.

Wednesday, June 29, 2022

Tuesday, June 28, 2022

EL DESASTRE DEL MERCADO DE 2022 (MATTHEW PIEPENBURG)

That is, we saw an: 1) inevitable liquidity crisis which would take our 2) zombie bond markets to the floor, yields (and hence interest rates) to new highs and 3) debt-soaked nations and markets tanking dangerously south into 4) the dark days of stagflation.

And that is precisely where we are today—no longer warning of a pending convergence of crises, but already well into a market disaster within the worst macro-economic setting (compliments of cornered “central planners”) that I have ever experienced in my post-dot.com career.

But sadly, and I do mean sadly, the worst is yet to come.

The Ignored Hangover

For well over a decade, the post-2008 central bankers of the world have been selling the intoxicating elixir (i.e., lie) that a debt crisis can be solved with more debt, which is then paid for with mouse-click money.

Investors drank this elixir with abandon as markets ripped to unprecedented highs on an inflationary wave of money printed out of thin air by a central bank near you.

In case you still don’t know what such “correlation” looks like, see below

For years, such free money from the global central banks ($35T and counting) has merely postponed rather than outlawed the hangover, but as we are seeing below, the hangover, and puking, has already begun in a stock, credit or currency market disaster near you.

Why?

Every Market Crisis is a Liquidity Crisis

Because the money (i.e., “liquidity”) that makes this drunken fantasy go round is drying up (or “tightening”) as the debt levels are piling up.

That is, years and years of issuing IOU’s (i.e., sovereign bonds) has made those IOU’s less attractive, and the solution-myth of creating money out of thin air to pay for those IOUs is becoming less believable as inflation rises like a killer shark from beneath the feet of our money printers.

The Most Important Bond in the World Has Lost Its Shine

As we’ve warned, the UST is experiencing a liquidity problem.

Demand for Uncle Sam’s bar tab (IOU’s) is tanking month, after month, after month.

As a result, the price of those bonds is falling and hence their yields (and our interest rates) are rising, creating massive levels of pain in an already debt-saturated world where rising rates kill drunken credit parties (i.e., markets).

Toward this end, Wall Street is seeing a dangerous rise in what the fancy lads call “omit days,” which basically means days wherein inter-dealer liquidity for UST’s is simply not available.

The Fed—Tightening into a Debt Crisis?

As all debt-soaked nations or regimes since the days of ancient Rome remind us , once debt levels exceed income levels by 100% or more, the only option left is to “inflate away” that debt by debasing (i.e., expanding/diluting) the currency—which is the very definition of inflation.

And that inflation is only just beginning…

Open & Obvious (i.e., Deadly) Bond Dysfunction

The West & Japan: Overplaying the Sanction Hand

As we warned in February, Russia is squeezing the sanction-makers with greater pain than history-and-math-ignorant “statesmen” like Kamala Harris could ever grasp.

From here in Europe, Western politicians are beginning to wonder if following the U.S. lead (coercion?) in chest-puffing was a wise idea, as gas prices on the continent skyrocket.

In this cold reality, the geniuses at the ECB are realizing that the very “state of their European Union” is at increasing risk of dis-union as citizens from Italy to Austria bend under the weight of higher prices and falling income.

As of this writing, the openly nervous ECB is thus inventing clever plans/titles to “fight fragmentation” within the EU by, you guessed it: Printing more money out of thin air to control bond yields and cap borrowing costs.

(By the way, such monetary policies are an open signal to short the Euro and GBP against the USD…)

Looking further east to that equally embarrassing state of the union in Japan, we see, as warned countless times, a tanking Yen out of a Japan that knows all too well the inflationary sickness that a non-stop money printer can create.

Like the UST, the Japanese JGB is as unloved as a pig in lipstick. Prices are falling and yields are rising.

By the way, and as part of our continued warning and theme of the slow process of de-dollarizationwhich the sanctions have only accelerated, it would not surprise us to see Japan making a similar “China-like” move to buy its Russian oil in its own currency rather than the USD.

Just saying…

Don’t Be (or buy) a Dip

As indicated above, trying to combat inflation with rate hikes is not only a joke, it creates a market disaster when a nation’s debt to GDP is at 120%.

To fight inflation, rates need be at a “neutral level,” (i.e., above inflation), and folks, that would mean 9% rates at the current 8%+ CPI level.

That aint gonna happen…

At $30T+ of government debt and rising, the Fed can NEVER use rising rates to fight inflation. End of story. The days of Volcker rate hikes (when public debt was $900B not $30T) are gone.

But the fickle Fed can raise rates high enough to kill a securities bubble and create “asset-bubble deflation,” which is precisely what we are seeing in real time, and this market disaster is only going to get worse.

In short, if you are buying this “dip,” you may want to think again.

As June trade tapes remind, the Dow dipped below 30000, and the S&P 500 reported an ominous 3666, already losing more than 20% despite remaining grossly over-valued as it slides officially into bear territory.

In short: These bear markets are not even close to their bottom, and today’s dip-buy may just be a trap, unless you think you can time a one-day rally amidst years of falling assets.

Markets won’t and don’t recover from the bear’s claws until spikes are well above two standard deviations. We are not there yet, which means we have much further to fall.

As we’ve warned, mean-reversion is a powerful force and we see deeper lows/reversions ahead:

Toward that end, we see an SPX which could easily fall at least 15% lower (i.e., to at least 1850) than the “Covid crash” of March 2020.

Based upon historic ranges, stocks won’t be anywhere near “fair value” until we see a Shiller PE at 16 or a nominal PE of 9-10.

In the 1970’s, for example, when we saw the S&P lose 48%, or even in 2008, when it lost 56%, U.S. debt to GDP levels were ¼ of what they are today. Furthermore, in the 1970’s the average consumer savings rate was 12%; today that rate is 4%.

Stated simply, the U.S., like the EU and Japan, is too debt-crippled and too GDP-broke to make this bear short and sweet. Instead, it will be long and mean, accompanied by stagflation and rising unemployment.

The Fed knows this, and is, in part, raising rates today so that will have something—anything—to cut in the market disaster tomorrow.

But that will be far too little, and far too late.

the real cause of the greatest market bubble and bust in the history of modern capital markets lies in the reflection of central bankers and politicians who bought time, votes, market bubbles, wealth disparity and cancerous inflation with a mouse-click.

History reminds us of this, current facts confirm it.

For now, the Fed will tighten, and thereby unleash an even angrier bear.

https://goldswitzerland.com/the-2022-market-disaster-more-pain-to-come/

Monday, June 27, 2022

ROE V. FERTILITY

(3)#Taiwan #ESTADISTICANACIMIENTOS#SUCESOSSIGMAX#ROEVFERTILITY

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 27, 2022

ALL THE "MEDIA" ARE FULL OF CORAGEOUS MESSAGES ON "ROE" OVERRULING

WE HAVE HERE AN "EX POST" #FERTILITY CATASTROPHE NO ONE IS DARING TO TALK ABOUT https://t.co/Ruof5p0LFK pic.twitter.com/hMN6pFeCYE

Sunday, June 26, 2022

DE QUIÉN SON LAS PÉRDIDAS DE LOS BANCOS CENTRALES (NO TAXATION WITHOUT REPRESENTATION)

Who owns the #Fed’s massive #losses? https://t.co/l3v9yrSS5i@MacleodFinance

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 24, 2022

Only the "citizens" and taxpayers

It is pure "taxation without representation"#newsovereign

SECTION 1. SHORT TITLE. This Act may be cited as the “No Taxation Without Representation Act”.

SEC. 2. FINDINGS. The Congress finds the following:

(1) The phrase “no taxation without representation” was a rallying cry of many American colonists during the period of British rule in the 1760s and early 1770s. The slogan gained widespread notoriety after the passage of the Sugar Act on April 5, 1764.

(2) American colonists increasingly resented having taxes levied upon them without having any legislators they elected who were voting in Parliament in London. The idea that there should be no taxation without representation dated back even further. Benjamin Franklin stated, “it is suppos’d an undoubted Right of Englishmen not to be taxed but by their own Consent given thro’ their Representatives.”

(3) This issue became even more defined in 1765 with the passage of the Stamp Act which was the first true attempt to levy a direct tax on the American colonies. Ultimately the tax was repealed, but the idea of no taxation without representation persisted.

(4) Article I, section 2, clause 1 of the United States Constitution, states, “The House of Representatives shall be composed of Members chosen every second Year by the People of the SEVERAL STATES, and the Electors in each State shall have the Qualifications requisite for Electors of the most numerous Branch of the State Legislature.”

(5) The Organic Act of 1801 placed Washington, DC, under the exclusive jurisdiction of the United States Congress and people in the District were no longer considered residents of Virginia or Maryland.

(6) Many in Washington, DC, were immediately opposed to the idea of being taxed without congressional representation and over the years several congressional leaders introduced constitutional amendments to give the District of Columbia voting representation, though none were successful.

(7) In 1898, Puerto Rico was acquired by the United States and currently has a Resident Commissioner with limited voting rights. Section 933 of the Internal Revenue Code of 1986 exempts bona fide citizens who are residents of Puerto Rico for the entire taxable year from Federal taxes on income earned in Puerto Rico.

(8) On March 31, 1917, the United States took possession of the Virgin Islands and in 1927, the territory’s residents were granted citizenship. Under section 932 of the Internal Revenue Code of 1986, individuals who are bona fide residents of the United States Virgin Islands during the entire taxable year, and who fully pay all income tax liabilities to the United States Virgin Islands, are not subject to Federal income taxes on their income.

(9) Guam was established as a territory of the United States after the passage of the Guam Organic Act of 1950. Under the provisions of section 935 of the Internal Revenue Code of 1986, residents of Guam are required to file tax returns with Guam, but not with the United States Federal Government and therefore the residents do not have to pay United States Federal income taxes.

(10) The Commonwealth of the Northern Mariana Islands was established in 1975 after residents decided not to pursue independence, but instead they opted to enter into territory negotiations. The tax treatment of the Northern Mariana Islands is similar to the structure of Guam in that bona fide residents are not required to pay Federal income taxes.

(11) American Samoa, which is technically considered “unorganized” because no Organic Acts have been passed by Congress, is governed by section 931 of the Internal Revenue Code of 1986. Under this section, bona fide year-round residents are exempt from Federal taxes on income they earn in Samoa, Guam, and Northern Mariana Islands, but are subject to Federal taxes on income earned elsewhere.

(12) In keeping with the early history and democratic traditions of the United States, the principles established in the Constitution, and in conformance with the other territories of the United States which have delegates but no Representative, the residents of the District of Columbia should be exempt from paying United States Federal income taxes.

SEC. 3. EXCLUSION FROM GROSS INCOME FOR INCOME FROM SOURCES WITHIN THE DISTRICT OF COLUMBIA.

(a) In General.—Subpart D of part III of subchapter N of chapter 1 of the Internal Revenue Code of 1986 is amended by adding at the end the following new section:

“(a) General Rule.—In the case of an individual who is a bona fide resident of the District of Columbia during the entire taxable year, gross income shall not include—

“(1) income derived from sources within the District of Columbia, and

“(2) income effectively connected with the conduct of a trade or business by such individual within the District of Columbia.

“(b) Deductions, Etc. Allocable To Excluded Amounts Not Allowable.—An individual shall not be allowed—

“(1) as a deduction from gross income any deductions (other than the deduction under section 151, relating to personal exemptions), or

“(2) any credit, properly allocable or chargeable against amounts excluded from gross income under this section.

“(c) Bona Fide Resident And Other Applicable Rules.—For purposes of this section, rules similar to the rules of section 876, 937, 957(c), 3401(a)(8)(D), and 7654 shall apply.”.

(b) Clerical Amendment.—The table of sections for subpart D of part III of subchapter N of chapter 1 of such Code is amended by adding at the end the following new item:

“Sec. 938. Income from sources within the District of Columbia.”

Friday, June 24, 2022

Dobbs v. Jackson Women’s Health Organization (24-06-2022: SCOTUS)

SUPREME COURT OF THE UNITED STATES

Syllabus

DOBBS, STATE HEALTH OFFICER OF THE MISSISSIPPI DEPARTMENT OF HEALTH, ET AL. v. JACKSON WOMEN’S HEALTH ORGANIZATION ET AL.

CERTIORARI TO THE UNITED STATES COURT OF APPEALS FOR THE FIFTH CIRCUIT

No. 19–1392. Argued December 1, 2021—Decided June 24, 2022

Mississippi’s Gestational Age Act provides that “[e]xcept in a medical emergency or in the case of a severe fetal abnormality, a person shall not intentionally or knowingly perform . . . or induce an abortion of an unborn human being if the probable gestational age of the unborn human being has been determined to be greater than fifteen (15) weeks.” Miss. Code Ann. §41–41–191. Respondents—Jackson Women’s Health Organization, an abortion clinic, and one of its doctors—challenged the Act in Federal District Court, alleging that it violated this Court’s precedents establishing a constitutional right to abortion, in particular Roe v. Wade, 410 U. S. 113, and Planned Parenthood of Southeastern Pa. v. Casey, 505 U. S. 833. The District Court granted summary judgment in favor of respondents and permanently enjoined enforcement of the Act, reasoning that Mississippi’s 15-week restriction on abortion violates this Court’s cases forbidding States to ban abortion pre-viability. The Fifth Circuit affirmed. Before this Court, petitioners defend the Act on the grounds that Roe and Casey were wrongly decided and that the Act is constitutional because it satisfies rational-basis review.

Held: The Constitution does not confer a right to abortion; Roe and Casey are overruled; and the authority to regulate abortion is returned to the people and their elected representatives. Pp. 8–79.

(a) The critical question is whether the Constitution, properly understood, confers a right to obtain an abortion. Casey’s controlling opinion skipped over that question and reaffirmed Roe solely on the basis of stare decisis. A proper application of stare decisis, however, requires an assessment of the strength of the grounds on which Roe was based. The Court therefore turns to the question that the Casey plurality did not consider. Pp. 8–32.

(1) First, the Court reviews the standard that the Court’s cases have used to determine whether the Fourteenth Amendment’s reference to “liberty” protects a particular right. The Constitution makes no express reference to a right to obtain an abortion, but several constitutional provisions have been offered as potential homes for an implicit constitutional right. Roe held that the abortion right is part of a right to privacy that springs from the First, Fourth, Fifth, Ninth, and Fourteenth Amendments. See 410 U. S., at 152–153. The Casey Court grounded its decision solely on the theory that the right to obtain an abortion is part of the “liberty” protected by the Fourteenth Amendment’s Due Process Clause. Others have suggested that support can be found in the Fourteenth Amendment’s Equal Protection Clause, but that theory is squarely foreclosed by the Court’s precedents, which establish that a State’s regulation of abortion is not a sex-based classification and is thus not subject to the heightened scrutiny that applies to such classifications. See Geduldig v. Aiello, 417 U. S. 484, 496, n. 20; Bray v. Alexandria Women’s Health Clinic, 506 U. S. 263, 273– 274. Rather, regulations and prohibitions of abortion are governed by the same standard of review as other health and safety measures. Pp. 9–11.

(2) Next, the Court examines whether the right to obtain an abortion is rooted in the Nation’s history and tradition and whether it is an essential component of “ordered liberty.” The Court finds that the right to abortion is not deeply rooted in the Nation’s history and tradition. The underlying theory on which Casey rested—that the Fourteenth Amendment’s Due Process Clause provides substantive, as well as procedural, protection for “liberty”—has long been controversial. The Court’s decisions have held that the Due Process Clause protects two categories of substantive rights—those rights guaranteed by the first eight Amendments to the Constitution and those rights deemed fundamental that are not mentioned anywhere in the Constitution. In deciding whether a right falls into either of these categories, the question is whether the right is “deeply rooted in [our] history and tradition” and whether it is essential to this Nation’s “scheme of ordered liberty.” Timbs v. Indiana, 586 U. S. ___, ___ (internal quotation marks omitted). The term “liberty” alone provides little guidance. Thus, historical inquiries are essential whenever the Court is asked to recognize a new component of the “liberty” interest protected by the Due Process Clause. In interpreting what is meant by “liberty,” the Court must guard against the natural human tendency to confuse what the Fourteenth Amendment protects with the Court’s own ardent views about the liberty that Americans should enjoy. For this reason, the Court has been “reluctant” to recognize rights that are not mentioned in the Constitution. Collins v. Harker Heights, 503 U. S. 115, 125. Guided by the history and tradition that map the essential components of the Nation’s concept of ordered liberty, the Court finds the Fourteenth Amendment clearly does not protect the right to an abortion. Until the latter part of the 20th century, there was no support in American law for a constitutional right to obtain an abortion. No state constitutional provision had recognized such a right. Until a few years before Roe, no federal or state court had recognized such a right. Nor had any scholarly treatise. Indeed, abortion had long been a crime in every single State. At common law, abortion was criminal in at least some stages of pregnancy and was regarded as unlawful and could have very serious consequences at all stages. American law followed the common law until a wave of statutory restrictions in the 1800s expanded criminal liability for abortions. By the time the Fourteenth Amendment was adopted, three-quarters of the States had made abortion a crime at any stage of pregnancy. This consensus endured until the day Roe was decided. Roe either ignored or misstated this history, and Casey declined to reconsider Roe’s faulty historical analysis. Respondents’ argument that this history does not matter flies in the face of the standard the Court has applied in determining whether an asserted right that is nowhere mentioned in the Constitution is nevertheless protected by the Fourteenth Amendment. The Solicitor General repeats Roe’s claim that it is “doubtful . . . abortion was ever firmly established as a common-law crime even with respect to the destruction of a quick fetus,” 410 U. S., at 136, but the great common-law authorities—Bracton, Coke, Hale, and Blackstone—all wrote that a postquickening abortion was a crime. Moreover, many authorities asserted that even a pre-quickening abortion was “unlawful” and that, as a result, an abortionist was guilty of murder if the woman died from the attempt. The Solicitor General suggests that history supports an abortion right because of the common law’s failure to criminalize abortion before quickening, but the insistence on quickening was not universal, see Mills v. Commonwealth, 13 Pa. 631, 633; State v. Slagle, 83 N. C. 630, 632, and regardless, the fact that many States in the late 18th and early 19th century did not criminalize pre-quickening abortions does not mean that anyone thought the States lacked the authority to do so. Instead of seriously pressing the argument that the abortion right itself has deep roots, supporters of Roe and Casey contend that the abortion right is an integral part of a broader entrenched right. Roe termed this a right to privacy, 410 U. S., at 154, and Casey described it as the freedom to make “intimate and personal choices” that are “central to personal dignity and autonomy,” 505 U. S., at 851.

Ordered liberty sets limits and defines the boundary between competing interests. Roe and Casey each struck a particular balance between the interests of a woman who wants an abortion and the interests of what they termed “potential life.” Roe, 410 U. S., at 150; Casey, 505 U. S., at 852. But the people of the various States may evaluate those interests differently. The Nation’s historical understanding of ordered liberty does not prevent the people’s elected representatives from deciding how abortion should be regulated. Pp. 11–30.

(3) Finally, the Court considers whether a right to obtain an abortion is part of a broader entrenched right that is supported by other precedents. The Court concludes the right to obtain an abortion cannot be justified as a component of such a right. Attempts to justify abortion through appeals to a broader right to autonomy and to define one’s “concept of existence” prove too much. Casey, 505 U. S., at 851. Those criteria, at a high level of generality, could license fundamental rights to illicit drug use, prostitution, and the like. What sharply distinguishes the abortion right from the rights recognized in the cases on which Roe and Casey rely is something that both those decisions acknowledged: Abortion is different because it destroys what Roe termed “potential life” and what the law challenged in this case calls an “unborn human being.” None of the other decisions cited by Roe and Casey involved the critical moral question posed by abortion. Accordingly, those cases do not support the right to obtain an abortion, and the Court’s conclusion that the Constitution does not confer such a right does not undermine them in any way. Pp. 30–32.

(b) The doctrine of stare decisis does not counsel continued acceptance of Roe and Casey. Stare decisis plays an important role and protects the interests of those who have taken action in reliance on a past decision. It “reduces incentives for challenging settled precedents, saving parties and courts the expense of endless relitigation.” Kimble v. Marvel Entertainment, LLC, 576 U. S. 446, 455. It “contributes to the actual and perceived integrity of the judicial process.” Payne v. Tennessee, 501 U. S. 808, 827. And it restrains judicial hubris by respecting the judgment of those who grappled with important questions in the past. But stare decisis is not an inexorable command, Pearson v. Callahan, 555 U. S. 223, 233, and “is at its weakest when [the Court] interpret[s] the Constitution,” Agostini v. Felton, 521 U. S. 203, 235. Some of the Court’s most important constitutional decisions have overruled prior precedents. See, e.g., Brown v. Board of Education, 347 U. S. 483, 491 (overruling the infamous decision in Plessy v. Ferguson, 163 U. S. 537, and its progeny). The Court’s cases have identified factors that should be considered in deciding when a precedent should be overruled. Janus v. State, County, and Municipal Employees, 585 U. S. ___, ___–___. Five factors Cite as: 597 U. S. ____ (2022) 5 Syllabus discussed below weigh strongly in favor of overruling Roe and Casey. Pp. 39–66.

(1) The nature of the Court’s error. Like the infamous decision in Plessy v. Ferguson, Roe was also egregiously wrong and on a collision course with the Constitution from the day it was decided. Casey perpetuated its errors, calling both sides of the national controversy to resolve their debate, but in doing so, Casey necessarily declared a winning side. Those on the losing side—those who sought to advance the State’s interest in fetal life—could no longer seek to persuade their elected representatives to adopt policies consistent with their views. The Court short-circuited the democratic process by closing it to the large number of Americans who disagreed with Roe. Pp. 43–45.

(2) The quality of the reasoning. Without any grounding in the constitutional text, history, or precedent, Roe imposed on the entire country a detailed set of rules for pregnancy divided into trimesters much like those that one might expect to find in a statute or regulation. See 410 U. S., at 163–164. Roe’s failure even to note the overwhelming consensus of state laws in effect in 1868 is striking, and what it said about the common law was simply wrong. Then, after surveying history, the opinion spent many paragraphs conducting the sort of factfinding that might be undertaken by a legislative committee, and did not explain why the sources on which it relied shed light on the meaning of the Constitution. As to precedent, citing a broad array of cases, the Court found support for a constitutional “right of personal privacy.” Id., at 152. But Roe conflated the right to shield information from disclosure and the right to make and implement important personal decisions without governmental interference. See Whalen v. Roe, 429 U. S. 589, 599–600. None of these decisions involved what is distinctive about abortion: its effect on what Roe termed “potential life.” When the Court summarized the basis for the scheme it imposed on the country, it asserted that its rules were “consistent with,” among other things, “the relative weights of the respective interests involved” and “the demands of the profound problems of the present day.” Roe, 410 U. S., at 165. These are precisely the sort of considerations that legislative bodies often take into account when they draw lines that accommodate competing interests. The scheme Roe produced looked like legislation, and the Court provided the sort of explanation that might be expected from a legislative body. An even more glaring deficiency was Roe’s failure to justify the critical distinction it drew between pre- and post-viability abortions. See id., at 163. The arbitrary viability line, which Casey termed Roe’s central rule, has not found much support among philosophers and ethicists who have attempted to justify a right to abortion. The most obvious problem with any such argument is that viability has changed over time and is heavily dependent on factors—such as medical advances and the availability of quality medical care—that have nothing to do with the characteristics of a fetus. When Casey revisited Roe almost 20 years later, it reaffirmed Roe’s central holding, but pointedly refrained from endorsing most of its reasoning. The Court abandoned any reliance on a privacy right and instead grounded the abortion right entirely on the Fourteenth Amendment’s Due Process Clause. 505 U. S., at 846. The controlling opinion criticized and rejected Roe’s trimester scheme, 505 U. S., at 872, and substituted a new and obscure “undue burden” test. Casey, in short, either refused to reaffirm or rejected important aspects of Roe’s analysis, failed to remedy glaring deficiencies in Roe’s reasoning, endorsed what it termed Roe’s central holding while suggesting that a majority might not have thought it was correct, provided no new support for the abortion right other than Roe’s status as precedent, and imposed a new test with no firm grounding in constitutional text, history, or precedent. Pp. 45–56.

(3) Workability. Deciding whether a precedent should be overruled depends in part on whether the rule it imposes is workable—that is, whether it can be understood and applied in a consistent and predictable manner. Casey’s “undue burden” test has scored poorly on the workability scale. The Casey plurality tried to put meaning into the “undue burden” test by setting out three subsidiary rules, but these rules created their own problems. And the difficulty of applying Casey’s new rules surfaced in that very case. Compare 505 U. S., at 881– 887, with id., at 920–922 (Stevens, J., concurring in part and dissenting in part). The experience of the Courts of Appeals provides further evidence that Casey’s “line between” permissible and unconstitutional restrictions “has proved to be impossible to draw with precision.” Janus, 585 U. S., at ___. Casey has generated a long list of Circuit conflicts. Continued adherence to Casey’s unworkable “undue burden” test would undermine, not advance, the “evenhanded, predictable, and consistent development of legal principles.” Payne, 501 U. S., at 827. Pp. 56–62.

(4) Effect on other areas of law. Roe and Casey have led to the distortion of many important but unrelated legal doctrines, and that effect provides further support for overruling those decisions. See Ramos v. Louisiana, 590 U. S. ___, ___ (KAVANAUGH, J., concurring in part). Pp. 62–63.

(5) Reliance interests. Overruling Roe and Casey will not upend concrete reliance interests like those that develop in “cases involving property and contract rights.” Payne, 501 U. S., at 828. In Casey, the controlling opinion conceded that traditional reliance interests were Cite as: 597 U. S. ____ (2022) 7 Syllabus not implicated because getting an abortion is generally “unplanned activity,” and “reproductive planning could take virtually immediate account of any sudden restoration of state authority to ban abortions.” 505 U. S., at 856. Instead, the opinion perceived a more intangible form of reliance, namely, that “people [had] organized intimate relationships and made choices that define their views of themselves and their places in society . . . in reliance on the availability of abortion in the event that contraception should fail” and that “[t]he ability of women to participate equally in the economic and social life of the Nation has been facilitated by their ability to control their reproductive lives.” Ibid. The contending sides in this case make impassioned and conflicting arguments about the effects of the abortion right on the lives of women as well as the status of the fetus. The Casey plurality’s speculative attempt to weigh the relative importance of the interests of the fetus and the mother represent a departure from the “original constitutional proposition” that “courts do not substitute their social and economic beliefs for the judgment of legislative bodies.” Ferguson v. Skrupa, 372 U. S. 726, 729–730.

The Solicitor General suggests that overruling Roe and Casey would threaten the protection of other rights under the Due Process Clause. The Court emphasizes that this decision concerns the constitutional right to abortion and no other right. Nothing in this opinion should be understood to cast doubt on precedents that do not concern abortion. Pp. 63–66.

(c) Casey identified another concern, namely, the danger that the public will perceive a decision overruling a controversial “watershed” decision, such as Roe, as influenced by political considerations or public opinion. 505 U. S., at 866–867. But the Court cannot allow its decisions to be affected by such extraneous concerns. A precedent of this Court is subject to the usual principles of stare decisis under which adherence to precedent is the norm but not an inexorable command. If the rule were otherwise, erroneous decisions like Plessy would still be the law. The Court’s job is to interpret the law, apply longstanding principles of stare decisis, and decide this case accordingly. Pp. 66–69.

(d) Under the Court’s precedents, rational-basis review is the appropriate standard to apply when state abortion regulations undergo constitutional challenge. Given that procuring an abortion is not a fundamental constitutional right, it follows that the States may regulate abortion for legitimate reasons, and when such regulations are challenged under the Constitution, courts cannot “substitute their social and economic beliefs for the judgment of legislative bodies.” Ferguson, 372 U. S., at 729–730. That applies even when the laws at issue concern matters of great social significance and moral substance. A law regulating abortion, like other health and welfare laws, is entitled to a “strong presumption of validity.” Heller v. Doe, 509 U. S. 312, 319. It must be sustained if there is a rational basis on which the legislature could have thought that it would serve legitimate state interests. Id., at 320.

Mississippi’s Gestational Age Act is supported by the Mississippi Legislature’s specific findings, which include the State’s asserted interest in “protecting the life of the unborn.” §2(b)(i). These legitimate interests provide a rational basis for the Gestational Age Act, and it follows that respondents’ constitutional challenge must fail. Pp. 76– 78.

(e) Abortion presents a profound moral question. The Constitution does not prohibit the citizens of each State from regulating or prohibiting abortion. Roe and Casey arrogated that authority. The Court overrules those decisions and returns that authority to the people and their elected representatives. Pp. 78–79. 945 F. 3d 265, reversed and remanded.

ALITO, J., delivered the opinion of the Court, in which THOMAS, GORSUCH, KAVANAUGH, and BARRETT, JJ., joined. THOMAS, J., and KAVANAUGH, J., filed concurring opinions. ROBERTS, C. J., filed an opinion concurring in the judgment. BREYER, SOTOMAYOR, and KAGAN, JJ., filed a dissenting opinion.

Thursday, June 23, 2022

EL MERCADO DE CRIPTOACTIVOS Y LA ESTABILIDAD FINANCIERA (III)

Citigroup has apparently received a warning from the SEC that if it builds a crypto platform and begins to act as a custodian for cryptocurrencies, it’s going to impact its balance sheet – which means that the Fed will also have to require it to hold more capital against risky assets. Citigroup reported the following on its quarterly filing (10-Q) with the SEC for the quarter ending March 31, 2022:

“In March 2022, the SEC issued Staff Accounting Bulletin (SAB) No. 121, which expresses the views of the SEC staff regarding the accounting for obligations to safeguard crypto-assets an entity holds for platform users. Specifically, the guidance requires issuers that hold digital assets for their platform users to recognize a liability for their obligation to safeguard the digital assets held and a corresponding asset, measured initially and subsequently at fair value. The guidance is effective for interim and annual periods ending after June 15, 2022, with retrospective application to the beginning of the fiscal year, with early adoption permitted. Citi is currently assessing the application of SAB 121, but based on its current activity does not expect any impact to its results of operations as a result of adopting SAB 121.”

EL MERCADO DE CRIPTOACTIVOS Y LA ESTABILIDAD FINANCIERA (II)

Estimates are that the real size of the crypto market is more in the range of $10 trillionhttps://t.co/ID8ISaznii https://t.co/WhaQNXjCh8

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 23, 2022

Estimates are that the real size of the crypto market is more in the range of $10 trillion. Anyone who thinks that a market of that size can implode without “significant macro-economic implications” is likely not an economist. (Unfortunately, Jerome Powell, the head of the monetary policy setting institution in the United States has a law degree, not an economics degree. And not to put too fine a point on it, but Powell was dead wrong on inflation being transitory and we’re all paying a steep price for that botched forecast.)

EL MERCADO DE CRIPTOACTIVOS Y LA ESTABLILIDAD FINANCIERA (I)

Is the #CryptoThreat to U.S. #FinancialStability $889 Billion or $10 Trillion? https://t.co/CgN3tU8IGJ

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 23, 2022

It is important to note the entire cryptocurrency market cap is $889.25 billion versus the American GDP, which is $25.34 trillion and an equities market more than $49 trillion

Powell responded that the Fed was watching those events “very carefully” but the Fed “did not see significant macro-economic implications.” The article goes on to lend credence to this observation from the Fed by noting the following:

“It is important to note the entire cryptocurrency market cap is $889.25 billion versus the American GDP, which is $25.34 trillion, and an equities market that controls more than $49 trillion.”

So exactly how big is the problem? The $889.25 billion market cap for crypto cited by Benzinga is a miniscule part of the problem. That’s just the market value of all of the crypto that trades. And it should be noted that the market cap of crypto stood at $2.7 trillion as of last November, so investors have already experienced a negative wealth effect of $1.8 trillion.

But what about all of the crypto mining stocks that went public and have now lost 70 to 90 percent of investors’ money? What about the loans taken out by the crypto mining companies to buy all of that energy-guzzling computer equipment? What about the billions of dollars in margin loans sitting at federally-insured banks that were made to hedge funds to leverage their crypto bets? What about the bank loans to venture capital firms to invest in hundreds of crypto startup firms?

Wednesday, June 22, 2022

EL DILEMA IMPOSIBLE DEL BANCO CENTRAL EUROPEO : INFLACIÓN Y DEUDA SOBERANA ESTADOS MIEMBROS (V)

David @david_hrzone · 20 jun. Respondiendo a @ph2403 @MishGEA y 3 másThey will create a common tax and budget in the end. There will be one European bond. Germany will give up.

— Philippe (@ph2403) June 20, 2022

EL DILEMA IMPOSIBLE DEL BANCO CENTRAL EUROPEO: INFLACIÓN Y DEUDA SOBERANA DE LOS ESTADOS MIEMBROS (IV)

#ecb

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 22, 2022

Mario Draghi got away with a bluff because the pressures of globalization were disinflationary.

Lagarde will not get away with the same bluff, stated very wimpishly, because the forces of de-globalization and the war in Ukraine are very inflationary. https://t.co/ha9aNeW7Mg

EL DILEMA IMPOSIBLE DEL BANCO CENTRAL EUROPEO: INFLACIÓN Y DEUDA SOBERANA DE LOS ESTADOS MIEMBROS (III)

#ecb https://t.co/ha9aNeW7Mg pic.twitter.com/xjwWGDJHsA

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 22, 2022

EL DILEMA IMPOSIBLE DEL BANCO CENTRAL EUROPEO: INFLACIÓN Y DEUDA SOBERANA DE LOS ESTADOS MIEMBROS (II)

#ecb https://t.co/ha9aNeW7Mg pic.twitter.com/nYgIyD6AwD

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 22, 2022

EL DILEMA IMPOSIBLE DEL BANCO CENTRAL EUROPEO: INFLACIÓN Y DEUDA SOBERANA DE ESTADOS MIEMBROS (I)

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 22, 2022What is happening between the markets and the central bank is not just a form of mutual miscommunication. This is a power struggle. The ECB is resisting what is known as fiscal dominance, which is when a central bank can’t follow its target because it is under pressure to bail out governments. There are no easy answers. The central bank knows it cannot ignore sovereign debt spreads, because they do affect monetary policy transmission mechanisms. The only instrument that would fix this problem is a mutualised eurobond. In other words, fiscal dominance is not so much a matter of choice, but one of a lack of alternatives. The ECB may well be stuck in this situation. Support the bond markets, and risk a permanent overshoot of the inflation target. Or don't support the bond market, and risk a sovereign-debt crisis, a financial meltdown.

Monday, June 20, 2022

HISTORY OF US EQUITY BEAR MARKETS (1890-2020)

#History #USEQUITY#BEARMARKETS

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 20, 2022

The past does not repeat itself. But it is rhyming. Do not ignore time’s poetry.#MARTINWOLF pic.twitter.com/srUpXzmleW

Friday, June 17, 2022

LA TORMENTA EN EL SECTOR BANCARIO (CUADROS, (III))

#alasdairmacleod#sectorbancario

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 17, 2022

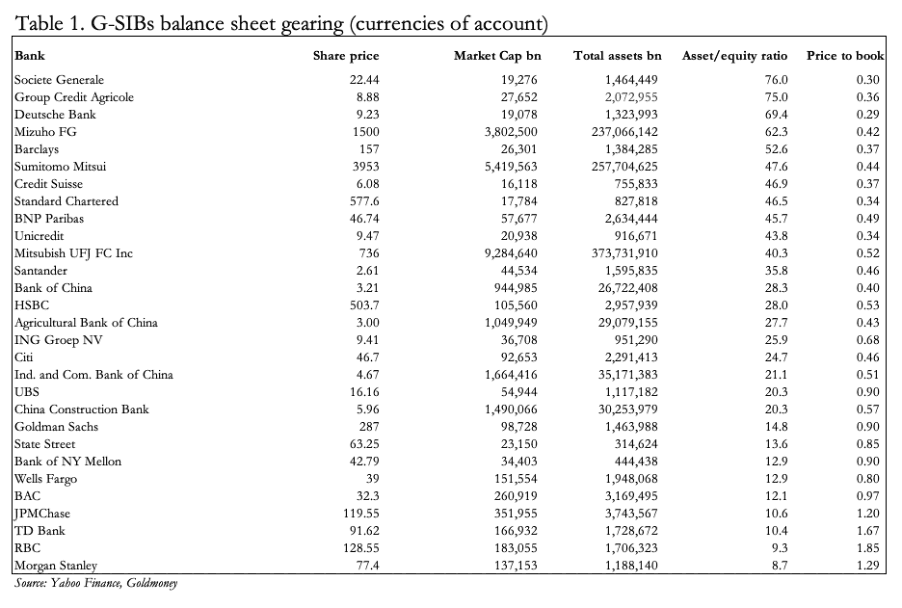

apalancamiento de bancos sistémicamente relevantes a nivel global y relación precio/valor contable

Macleod señala la relativa mejor posición de los bancos USA

sobre sus activos y riesgos puede verse no obstantehttps://t.co/M4Zf7flIfC pic.twitter.com/46ZVf9Jy7d

LA TORMENTA EN EL SECTOR BANCARIO (CUADROS, (II))

#alasdairmacleod#sectorbancario

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 17, 2022

(2)

rentabilidad de deuda pública de la eurozona a 10 años y caída de valor-por país pic.twitter.com/k5FBMOIQ48

LA TORMENTA EN EL SECTOR BANCARIO (CUADROS, I)

#alasdairmacleod#sectorbancario

— Guillermo Ruiz Zapatero (@ruiz_zapatero) June 17, 2022

(1) pic.twitter.com/qfoh5022h7

Thursday, June 16, 2022

LA TORMENTA EN EL SECTOR BANCARIO (ALASDAIR MACLEOD, 16-06-2022)

A perfect storm in banking is brewing

Jun 16, 2022·Alasdair MacleodWhy are markets crashing?

How to recapitalise a central bank

The G-SIBs’ balance sheets have deteriorated significantly

The ECB’s impossible position

At the end of 2021, the ECB’s balance sheet showed assets of €8,466bn and share capital of €109bn. That’s a ratio of assets to shareholder capital of 78 times. A high ratio is tolerable for a central bank so long as it sticks to issuing bank notes. But by last December the ECB had also accumulated Eurozone government and other bonds totalling €4,886bn.

Since the year-end, by last Friday the value of these bonds has fallen sharply, as shown in Table 2, of selected 10-year Eurozone government bonds.

Bank of Japan is in deepening trouble

The Bank of Japan is trying to save itself from further financial embarrassment by ensuring bond yields rise no further. It has drawn a line in the sand for the 10-year JGB yield at 0.25% and has cleaned out the market at this maturity. The price is now in Humpty Dumpty territory: what the BoJ says is the price, is the price.

The cost has been yen weakness, which is now accelerating. Figure 1 shows the chart of the yen priced in US dollars.

The Bank of England has dug a hole for itself as well

How will the Fed respond to global problems?

Wednesday, June 15, 2022

Saturday, June 11, 2022

EL INFORME DE CONFLICTO DE LA COMISIÓN CONSULTIVA DE 18-05-2022 (IVA)

"Artículo 9.

(…)

A efectos de lo dispuesto en esta Ley, se considerarán

sectores diferenciados de la actividad empresarial o profesional los

siguientes:

a') Aquellos en los que las actividades económicas realizadas

y los regímenes de deducción aplicables sean distintos.

Se considerarán actividades económicas distintas aquellas que

tengan asignados grupos diferentes en la Clasificación Nacional de Actividades

Económicas.

(…)

Los regímenes de deducción a que se refiere esta letra a') se

considerarán distintos si los porcentajes de deducción, determinados con

arreglo a lo dispuesto en el artículo 104 de esta Ley, que resultarían aplicables

en la actividad o actividades distintas de la principal difirieran en más de 50

puntos porcentuales del correspondiente a la citada actividad principal.

La actividad principal, con las actividades accesorias a la

misma y las actividades económicas distintas cuyos porcentajes de deducción no

difirieran en más 50 puntos porcentuales con el de aquélla constituirán un solo

sector diferenciado.

Las actividades distintas de la principal cuyos porcentajes de

deducción difirieran en más de 50 puntos porcentuales con el de ésta

constituirán otro sector diferenciado del principal.

A los efectos de lo dispuesto en esta letra a'), se

considerará principal la actividad en la que se hubiese realizado mayor volumen

de operaciones durante el año inmediato anterior.

(…)

Artículo 101. Régimen de deducciones en sectores

diferenciados de la actividad empresarial o profesional.

Uno. Los

sujetos pasivos que realicen actividades económicas en sectores diferenciados

de la actividad empresarial o profesional deberán aplicar separadamente el

régimen de deducciones respecto de cada uno de ellos.

La

aplicación de la regla de prorrata especial podrá efectuarse independientemente

respecto de cada uno de los sectores diferenciados de la actividad empresarial

o profesional determinados por aplicación de lo dispuesto en el artículo 9,

número 1.º, letra c), letras a'), c') y d') de esta Ley.

Los

regímenes de deducción correspondientes a los sectores diferenciados de

actividad determinados por aplicación de lo dispuesto en el artículo 9, número

1.º, letra c), letra b') de esta Ley se regirán, en todo caso, por lo previsto

en la misma para los regímenes especiales simplificado, de la agricultura,

ganadería y pesca, de las operaciones con oro de inversión y del recargo de

equivalencia, según corresponda."

La aplicación de un régimen legal previsto especialmente (sectores diferenciados de actividad exenta y actividad sujeta en el IVA), o la consecución de sus efectos propios en el citado impuesto, no debería considerarse como un supuesto del art. 15 de la LGT.

Un efecto legalmente establecido no puede considerarse notoriamente artificioso o impropio ni un ahorro fiscal indebido (presupuestos del art.15 LGT)