Why are markets crashing?

Contracting bank credit always ends in a

crisis of some sort. With a long-term average of ten years, this cycle

of bank credit has been exceptionally long in the tooth. Before we even

consider the specific factors behind a withdrawal of credit, we can

assume that the longer the period of credit expansion that precedes it,

the greater the slump in economic activity that follows.

Whenever the dollar slipped, by lowering

interest rates instead of raising them the Fed could encourage foreign

portfolio buying. Lower interest rates increased flows of currency and

credit into financial assets instead of debasing the currency in the

non-financial economy.

Thus, the creation of extra bank credit was

directed increasingly into financial speculation in bond and equity

markets. There were bubbles, such as the dotcoms in the late-1990s and

in mortgage financing preceding the financial crisis of 2008/09. Despite

these interruptions, the US authorities made sure that global

investment flows primarily supported US financial interests.

As markets caught on, interest rates

declined to the point where they disappeared altogether. But as Triffin

observed, policies to ensure that a currency is available as the world’s

reserve are economically destructive in the long run, and the whole

trend set in motion from London’s big bang onwards has now concluded

with rising interest rates. It amounts to a super cycle of bank credit

expansion certain to end more dramatically than a single cycle.

Therefore, this bear market and its systemic issues can be expected to

be of a greater magnitude than those which followed the dotcoms and the

Lehman failure.

With interest rates so far beneath the rate

at which prices are rising, which is mainly the consequence of earlier

monetary debasement, losses are now accumulating for all those who

bought into the financialisation story and have failed to bail out of

it. Top of a hubristic list are the central banks themselves which

augmented monetary expansion with the acquisition of substantial bond

portfolios through quantitative easing. Those assets are now collapsing

in value, wiping out central bank equity many times over. The central

banks themselves will need recapitalising before they can tackle the

problems of a widespread systemic collapse in the commercial banking

network.

How to recapitalise a central bank

The Fed recently admitted that unrealised

losses on the bonds on the asset side of its balance sheet stood at

$330bn at end-March, which wipes out its balance sheet equity of $50bn

more than six times over. Since then, bond yields have risen a further

1%, increasing the deficit to closer to $500bn. But in the Fed’s case,

two differences from other central banks should be noted. First, the

profile of US Treasury debt is shorter term in average maturity than in

other advanced economies with high levels of government debt, confirmed

by the Fed’s intention to retain debt to maturity rather than selling

it. This means that price volatility is lessened. And secondly, some of

the debt is agency debt (Fanny Mae, Ginny Mae, and Freddy Mac) which on

early mortgage redemptions distributes payments to mortgage-backed

securities holders. In effect, the maturity profile is shortened by

these repayments, increasing their yield, and reducing their notional

volatility

But the Bank of Japan and the ECB are in an

entirely different situation. And so their ability to underwrite their

commercial banking networks is extremely impaired.

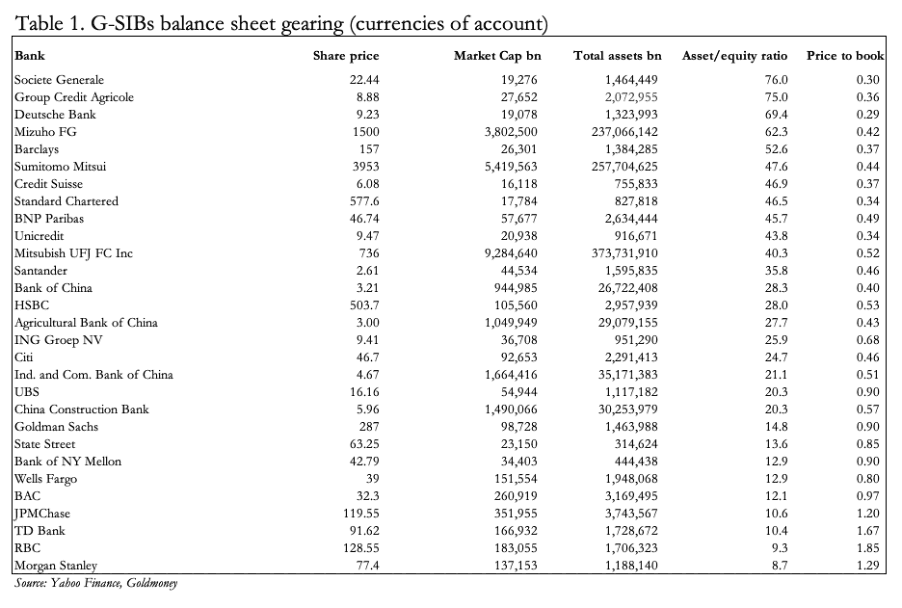

The G-SIBs’ balance sheets have deteriorated significantly

To see any banks with asset to equity

ratios for their ordinary shareholders of more than twenty times, let

alone the two French G-SIBs which appear to be over seventy, is simply

jaw-dropping.

Of particular concern is the bunching of

risk, with the Eurozone’s G-SIB cohort most vulnerable to shocks,

closely followed by the three Japanese banks. That banks in these two

jurisdictions are the most highly leveraged groups is partly a

consequence of negative interest rates. Credit margins have been tightly

compressed, and so long as banking regulations are complied with, the

management of these banks have been encouraged to maintain profitability

by increasing credit leverage.

Furthermore, as discussed below, the

European Central Bank and the Bank of Japan themselves will need to be

recapitalised if they are to underwrite the losses in the commercial

banking sector which are certain to quickly develop as interest rates

rise and bank credit contracts.

The ECB’s impossible position

Economic reality and the ECB’s monetary

policies have only occasionally had a tangential relationship, with the

ECB bullying its way over markets. The falsity of its position is now

being exposed.

Clearly, non-performing loans are rapidly

becoming an issue. Additionally, energy, food, and escalating producer

prices will make the situation far worse in the coming months. The

ability of the Eurozone’s banks to survive all these headwinds will be

increasingly questioned. The news here is exceedingly grim, with balance

sheet common equity to asset ratios in the stratosphere for the

Eurozone G-SIBs. Local banks, upon which most of the non-financial

burden of Eurozone credit defaults will fall will not be so highly

leveraged, being run by sensible local and regional managers in the

main. But in the deteriorating conditions the Eurozone now faces, even

asset to equity ratios of as little as ten times could prove fatal to a

bank’s future.

With respect to their underlying

shareholders, the Eurozone’s G-SIBs are the most highly leveraged

banking cohort. In the face of rising interest rates and the contraction

of bank credit, there can be little doubt that the first G-SIB failures

are likely to be among these banks. The ability of the ECB and its

network of shareholding national central banks to weather a credit storm

will be challenged and almost certainly found wanting.

At the end of 2021, the ECB’s balance

sheet showed assets of €8,466bn and share capital of €109bn. That’s a

ratio of assets to shareholder capital of 78 times. A high ratio is

tolerable for a central bank so long as it sticks to issuing bank notes.

But by last December the ECB had also accumulated Eurozone government

and other bonds totalling €4,886bn.

Since

the year-end, by last Friday the value of these bonds has fallen

sharply, as shown in Table 2, of selected 10-year Eurozone government

bonds.

But just assuming an average loss of 25% on

its bond holdings as of end-December, there is a loss to the ECB’s

assets from this source alone of €1,222bn. That’s a valuation write-off

of over eleven times the ECB’s capital account.

A recapitalisation of the ECB is due as a

matter of urgency before it is called upon along with the relevant

national central banks (NCBs — which are similarly insolvent) to

undertake the rescue of the Eurozone’s G-SIBs. We can see from their

exceptionally high gearing that they are likely to be the first victims

of bank credit contraction.

There are no easy options. It is possible

to conceive of a systemic failure at the central bank level threatening

the existence of the euro itself. Certainly, the foreign exchanges are

likely to be brutal in this matter.

Bank of Japan is in deepening trouble

The Bank of Japan has been conducting QE

since 2000, and to date has accumulated 80% of the country’s ETFs

amounting to 52 trillion yen ($420bn), as well as 538 trillion yen ($3.7

trillion) in bond purchases.It appears that these investments are

carried at cost on the BoJ’s balance sheet. The combined losses amount

to approximately 14 trillion yen ($104bn) since the year-end compared

with balance sheet capital consisting of equity and reserves of 4.7

trillion yen (USD35bn). That’s a rapidly rising ratio of net liabilities

to capital of 3:1.

The Bank of Japan is trying to save

itself from further financial embarrassment by ensuring bond yields rise

no further. It has drawn a line in the sand for the 10-year JGB yield

at 0.25% and has cleaned out the market at this maturity. The price is

now in Humpty Dumpty territory: what the BoJ says is the price, is the

price.

The cost has been yen weakness, which is now accelerating. Figure 1 shows the chart of the yen priced in US dollars.

However, permitting yen interest rates to

rise will lead to further problems for Japan’s commercial banks, which

at equity shareholder level are very highly leveraged, as the table

below illustrates.

The Bank of England has dug a hole for itself as well

How will the Fed respond to global problems?

a Fed funds rate of1.5%—1.75% is still a

long way behind the curve. They are bound to go considerably higher,

collapsing bond and financial collateral values. It will lead to a

crisis in financial markets. And given that the commercial banks in the

Eurozone and Japan possess extremely high shareholder leverage, that can

be expected to occur very soon.

Unless the Fed is prepared to let markets

sort this mess out — a course of action we can dismiss out of hand — the

Fed’s only possible response will be to inflate the dollar to

compensate for the contraction of bank credit. The means by which this

will be done is not the point. There will be no alternative, as the

Fed’s priority will be to save the financial system and to minimise the

consequences for the wider American economy and particularly for the

Federal Government’s finances. The other central banks mentioned in this

article will have to follow suit, where they can. Expect swap lines

between them to be expanded to enable them to do so. Expect bond markets

to be closed by diktat, perhaps for more than a day or two. As helpless

bystanders, we will all be looking into an abyss, fearful that there is

no resolution to an unsolvable crisis.

The outturn could be very different, but

logic suggests the following. Interest rates will rise until bank

failures materialise. Meanwhile, financial assets will have fallen in

value, possibly very quickly. Then we can expect monetary policy to

expand to rescue the commercial banks, supress bond yields and to

finance soaring government deficits.

At this side of the crisis, which is only

in its initial stages, the euro is slated as the first currency to

collapse entirely, not just because it is a fiat designed by committee,

but because of the depth of the structural problems in the ECB and its

shareholders.

Will the authorities respond by suppressing

prices like latter day Diocletians, banning gold ownership as well?

These would be stupid moves, but extremely likely. Gold markets could be

simply closed, denying access to those belatedly fleeing fiat.

No comments:

Post a Comment