THE UNHAPPY ENDING OF THE WHOLE AI DREAM

While I was waiting for Oracle numbers, a very interesting headline came out: “China plans $295bn state-directed AI buildout as Beijing moves to lock out Nvidia and AMD”.

This is what I wrote about 8 months ago in “THE DATA CENTERS FRENZY WILL BE REMEMBERED AS THE LARGEST WASTE OF CAPITAL IN HISTORY”:

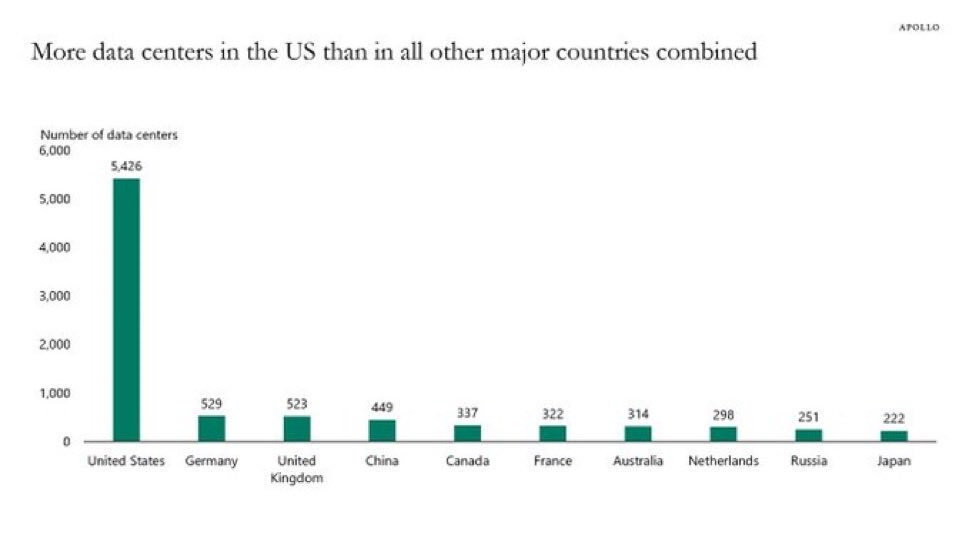

“As you can see in this chart, the number of data centers operational in the US right now is greater than all other countries combined and ten times higher than Germany, the second country by number of data centers.”

“Yet, nobody sees anything wrong with this. Let me ask a question: if there is a global AI arms race ongoing, then why aren’t all other countries participating?”

China, a country of 1.4 billion people and the second largest economy in the world, just committed to spending on building data centers over the next 5 years, roughly the same amount Google alone is expected to spend in one year. Furthermore, the strict condition to build data centers will be using 80% or more of domestically produced semiconductors. Is China doing this to protect Huawei and its other domestic companies, or is there something very wrong with how the whole AI data center buildout in the US around Nvidia, AMD GPUs at first, and now other alternatives like Google TPUs is developing? Of course, there is something very wrong with what has been happening in the US for many years now, and it never took a genius to figure that out; all that was needed was paying attention because the numbers never made any freaking sense.

Now that investors are starting to ask one simple question, “Why are you still not making much money after we gave you hundreds of billions of capital?”, you can notice all they can answer is “Trust me, bro.” This behavior is, unfortunately, not what lenders like to hear. Not surprisingly, you can observe how more and more companies are being refused new requests to borrow money and are instead forced to raise cash by issuing equity. Those that will still be able to entice lenders and not dilute their capital will only be companies with a sustainable business that can sustain an increasing debt burden.

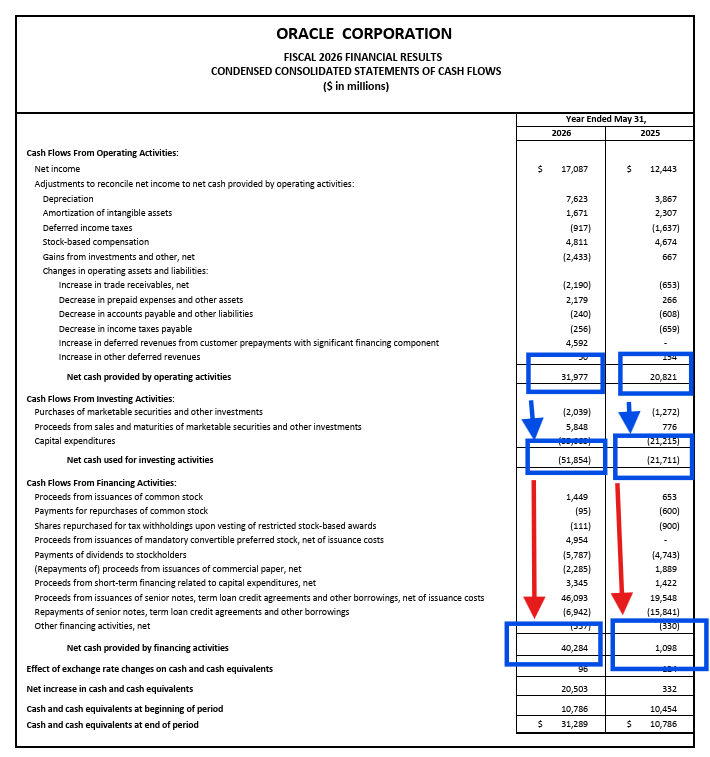

Oracle is the most glaring example among all; just compare the cash flow numbers between FY 2025 and the FY 2026 just reported

In one column, you can see a software company venturing carefully into a new business. In the other column, you can see an infrastructure company with a software business attached to it. With the exception of Apple, you can observe the exact same trend among all the major tech mega-cap companies.

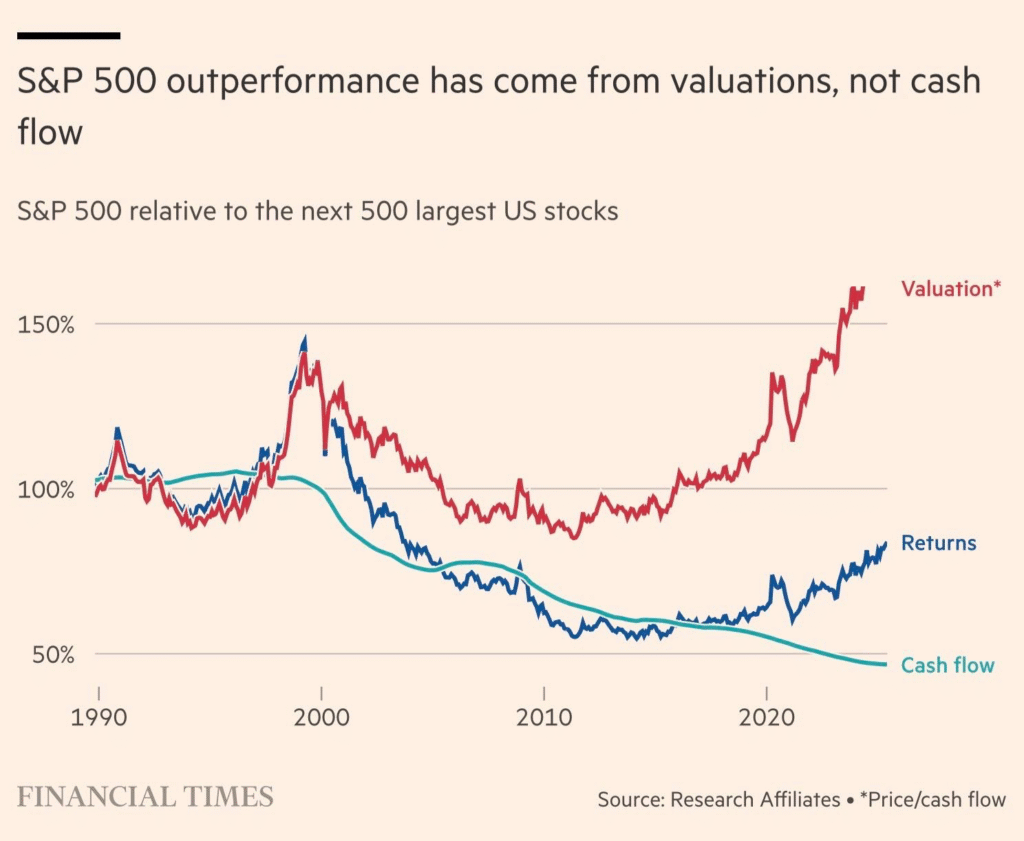

This great chart from the FT perfectly summarizes what I just described:

No comments:

Post a Comment